Within the Marketplace solution, the payout concept is the transfer of funds to the Marketplace Operator and the Submerchants. Funds are transferred via bank transfer SEPA CT, which implies that all entities registered in the Marketplace (Marketplace Operator and Submerchants) must held bank accounts within the Single Euro Payments Area (SEPA).

The payout timing can be scheduled, on demand or a combination of the previous two. The payout scheduling request process is triggered by the Marketplace Operator via Split API and can be later rescheduled, when applicable. If the Marketplace Operator does not specify a payout date on the API request, the system will consider the payout date defined in SIBS Backoffice, at the Submerchant’s page/register.

Marketplaces, also known as “digital supermarkets”, have become increasingly popular, providing consumers with an experience comparable to walking into a department store and visiting dozens of shops across all sectors with the comfort of avoiding the physical travelling to the location and using a single centralised platform. This type of solution optimises the user experience, allowing the user to choose from a greater range of products across multiple Merchants and make a single payment.

Following the growing interest of consumers and the needs identified in this area, SIBS developed an innovative and complete multi-channel Marketplace solution, which brings together the features and benefits of several marketplaces on a central processing platform, providing it with the latest trends in payment technology.

SIBS Marketplace solution is a multi-channel, multi-brand processing platform (Visa, Mastercard, UPI and MB), which brings together features of SIBS Payment Gateway (SPG), as well as the physical POS, SmartPOS and mPOS solutions, and is equipped with the latest trends in payment technology.

This solution allows the Merchant to expand its business as a Marketplace Operator, enabling integration with agents, resellers and/or service providers (referred to as ‘Submerchants’), accepting payments on their behalf. It also allows to split payments, transfer funds and pay to Submerchants, providing full control over the buyer and seller experience. In addition, it enables its users to remain compliant with new regulations, such as PSD21, and in line with the latest payment trends. The figure shows a summary diagram of the solution’s operation.

Benefits

Onboarding and KYC

The solution ensures compliance with local and international regulatory requirements, such as sub-merchant anti-money laundering (AML) and Know Your Customer (KYC) guidelines, which is vital for transactions.

Escrow account

Submerchant funds are held temporarily at a third party neutral account, awaiting the day of payment. Once all conditions have been met, the Marketplace Operator requests the payment split and funds are released to submerchants.

Payment split

Splits can be made transaction by transaction or in bulk, always via API. The amounts and commissions to be distributed are fully customized by the Marketplace Operator.

Payouts

Payouts are processed on demand or can be scheduled daily, weekly or monthly.

Funds transfer

Secure transfer of funds between the various parties involved. The transfer of funds will be processed via SEPA CT, respecting the processing and clearing timings of this service.

Marketplace reporting

The solution provides a free daily report with the details and status of splits and payouts.

The data and documents required for the KYC process are based on the Portuguese regulation “Aviso do Banco de Portugal no. 5/2013”. The fields for registering a Submerchant type “Individual Person” are listed below.

The onboarding of Submerchants must be carried out by the Marketplace Operator, via API or manually in SIBS Backoffice, The Acquirer of the solution will have access to all the information and documentation needed for the KYC process also via API or SIBS Backoffice.

Personal data

Taxpayer Identification Number (TIN) / Fiscal number

Name

Date of birth

Birth place

Nationality

Profession

Employer

IBAN

BIC

Permanent Residence address: Location, ZIP code, Country

Tax address, if different from Permanent Residence address: Location, Zip code, Country

General data

Taxpayer Identification Number (TIN) / Fiscal Number of the company, if different

Denomination

Object

Headquarters address, if different from the other addresses: Location, Zip code, Country

Email

Telephone

Identify documents

This information must be entered per each nationality, if the Individual Person has more than one nationality.

The data and documents required for the KYC process are based on the Portuguese regulation “Aviso do Banco de Portugal no. 5/2013”. The fields for registering a Submerchant type “Corporate Person” are listed below.

Please note that the information presented is generic and may vary according to the country of the Submerchant or in some specific cases.

The onboarding of Submerchants must be carried out by the Marketplace Operator, via API or manually in SIBS Backoffice. The Acquirer of the solution will have access to all the information and documentation needed for the KYC process also via API or SIBS Backoffice.

General data

Taxpayer Identification Number (TIN) / Fiscal Number;

Pursuant to the payment industry regulation in force, the Acquirer of a Marketplace is required to know all the players on the platform, including all Submerchants as well as the Marketplace Operator.

If deemed appropriate by the Acquirer, a Know Your Customer (KYC) verification check process is carried out for all Submerchants operating on the platform, as well as for Marketplace Operators. KYC is the process by which the Acquirers of the solution validate the Submerchants’ identity in the Marketplace solution.

Marketplace operator

The KYC process for the Marketplace Operator begins when the Merchant contracts the acceptance of payments with an Acquirer. This process is handled directly with the Acquirer and precedes the start of the Marketplace operation.

Submerchant

Verification requirements differ in accordance to each Submerchant legal entity type, i.e. Corporate Person or Individual Person. The Marketplace Operator must register each Submerchant on the Marketplace solution. Submerchant data is then shared with the Marketplace Acquirer who verifies and defines whether to approve/activate them or not. Only active Submerchants are eligible for payouts.

SIBS intends to take a broader position in the e-commerce market and allow access to payment solutions for Marketplace, in order to include in this component the various payment methods already available, in addition to other features, such as the possibility of releasing the funds to the players at the time of the actual purchase, or the onboarding of a large number of Submerchants in a digital way. SIBS Marketplace solution provides a backoffice for the Marketplace Operator (platform owner) and its Submerchants, so that they can manage and control commercial transactions in real time.

SIBS has developed a payment gateway (SIBS Payment Gateway [SPG]), which supports both International Payment Systems (Visa, Mastercard and UPI) as well as the domestic MB scheme (MULTIBANCO), Private Networks and other payment methods. SPG is integrated with SIBS Backoffice, a platform that is used as the backoffice for all players involved (Marketplace Operators and Submerchants) and also enables the onboarding1 of Submerchants, a task carried out by the Marketplace Operators.

Physical Solutions

On the physical Marketplace side, integration is carried out through SmartPOS, mPOS or POS solutions as payment terminals. These solutions are associated with SIBS Backoffice, a platform that is used as the backoffice for all players involved (Marketplace Operators and Submerchants) and also enables the onboarding of Submerchants, a task carried out by the Marketplace Operators.

The integration of SmartPOS in the physical Marketplace results in a complete solution, which allows combining the payment operations of a traditional POS (Point-of-Sales) with the capabilities of a smartphone. Within the SmartPOS app store, Merchants have several apps available that allow them to perform inventory management, user management, invoicing, among other features. Through SmartPOS Merchants can accept payments (domestic and international cards and MB WAY), and also manage their business, increasing the value of their services through a device that promotes integrability and mobility.

If they choose mPOS as a complement to the physical Marketplace, Merchants provide their customers with a more integrated and mobile payment experience compared to a traditional POS. In this case, the purchase is made through a mobile app installed on a smartphone or tablet that communicates wirelessly with a card reader.

Besides the SmartPOS and mPOS solutions, Merchants can also opt for the traditional POS solution as a complement to the physical Marketplace, providing their customers with a payment terminal they are already familiar with.

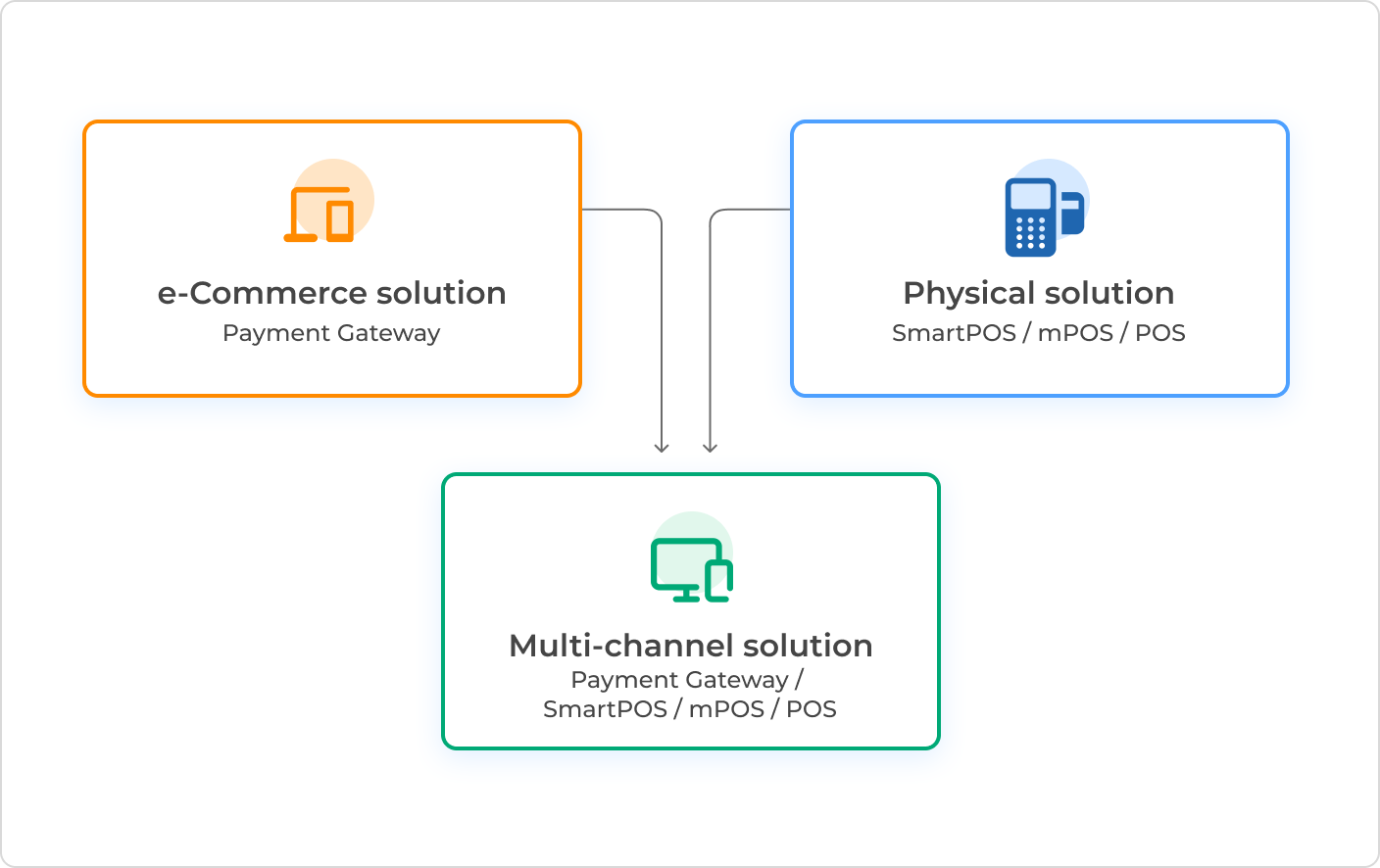

Multi-Channel Solutions

This component involves the joining of physical and digital (e-commerce) Marketplace solutions, allowing the availability of a single product of wide range. The multi-channel solution integrates physical and digital POS in a centralised Marketplace, with only one single Marketplace Operator. Similarly to the e-commerce solutions, the PGS will be the terminal used for e-commerce purchases, while the SmartPOS, mPOS and POS will be the terminals used for physical purchases.

Process description

The Marketplace Operator contracts the solution with an EAT/Acquirer

Once the solution has been contracted, the EAT registers the Marketplace Operator in SIBS systems and the Acquirers register the respective agreements

The Marketplace Operator collects KYC data from Submerchants and, via SIBS Backoffice or via API, sends this data for validation to the respective Acquirers (for further details, please refer to section 3.1.1.1)

Submerchants may start transacting in accordance with the conditions agreed between the Marketplace Operator and the Acquirers

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.